Table of Content

- FAQs about mortgage interest rates

- What Are the Mortgage Rate Trends for 2022?

- Experts’ Take on Current Mortgage Rates

- How long do you have to live in a house with a VA loan?

- How is my mortgage rate determined?

- Non-conforming mortgages

- How to Calculate the Effective Interest Rate?

- Additional refinancing resources

If inflation continues to increase and rates continue to climb, it will likely translate to higher interest rates -- and steeper monthly mortgage payments. As such, you may have better luck locking in a lower mortgage interest rate sooner rather than later. No matter when you decide to shop for a home, it's always a good idea to seek out multiple lenders to compare rates and fees to find the best mortgage for your specific situation.

Because you have lower payments, you can qualify for a bigger loan and a more expensive house. You can save thousands of dollars over the life of your mortgage by getting multiple offers. Mortgage rates have been on a wild ride as of late, with the 30-year fixed now past the once-unthinkable threshold of 7 percent as the Federal Reserve cracks down on inflation.

FAQs about mortgage interest rates

We value our editorial independence and follow editorial guidelines. Funding offers competitive bridging loans for homeowners who want to buy their next property sooner. While the Reserve Bank sets the floor for certain interest rates, banks and lenders have a lot of flexibility to price interest rates themselves.

You have to look for news about the different lenders online, read up on their history and check out reviews of the services and products they offer. You can also contact mortgage brokers or experts to find out information about any lender. There are many companies online that rank lenders offering VA loans, nationally and in your local area, and provide daily interest rates information.

What Are the Mortgage Rate Trends for 2022?

If the prime interest rate drops – as it has recently – the amount paid on your home loan will also decrease. The time frame of your credit history is also considered, as well as how many account applications have been submitted, and new accounts opened. Finder.com.au has access to track details from the product issuers listed on our sites.

Other lenders' terms are gathered by Bankrate through its own research of available mortgage loan terms and that information is displayed in our rate table for applicable criteria. Represent the weekly average interest rate among top offers within our rate table for the loan type and term selected. Use our rate table to view personalized rates from our nationwide marketplace of lenders on Bankrate. We use information collected by Bankrate, which is owned by the same parent company as CNET, to track daily mortgage rate trends.

Experts’ Take on Current Mortgage Rates

In addition to a lower rate, you could save by eliminating PMI, or tap your home’s equity via a cash-out refinance. Even if rates are low, however, it’s important to consider your future plans. If you expect to sell your home in the foreseeable future, for instance, it might not make sense to start over with a new loan. If you need money for renovations, a cash-out refi offers relatively cheap capital.

In the table above, you can see the lowest variable and fixed interest rates currently available on Finder. And you can compare them to the average fixed and variable interest rates from across Finder's entire home loan database. When picking a mortgage, it is important to pick out a loan term or payment schedule.

How long do you have to live in a house with a VA loan?

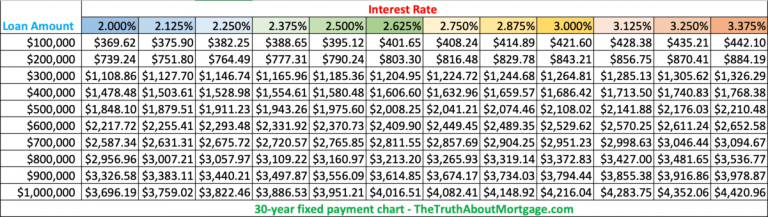

You also need to factor in maintenance and upkeep costs with owning a home. Secured loan where the property – often your home – is the collateral. So you’ll never be able to take out a mortgage without having some sort of real estate attached to it. Mortgage loans are issued by banks, credit unions, and other different types of lenders. The longer your mortgage’s repayment period, the more interest you’ll pay overall. Here’s what you’d pay in interest for a $300, year fixed rate mortgage at 4.5% and 5.5%, according to NextAdvisor’s mortgage calculator.

Thirty-year fixed mortgages are the most commonly sought out loan term. A 30-year fixed rate mortgage has a lower monthly payment than a 15-year one, but usually has a higher interest rate. Variable-rate mortgages can have lower interest rates upfront, but fluctuate over the term of your loan based on broader economic factors. How frequently a variable-rate mortgage changes is based on the loan’s terms. For example, a 5/1 ARM (adjustable-rate mortgage) would have a fixed rate for the first five years of the loan, then change every year after that.

A 30-year mortgage might be the right choice for you if a 15-year mortgage is out of your budget or if you’d like to be able to save some cash while making mortgage payments at the same time. It also gives the borrower a longer window to decide whether they want to sell down the road and pay off the mortgage. They also have the option to refinance into a shorter term loan or one with a lower interest rate if rates drop.

Any missed or delayed payments will affect your credit history, even if you make a double payment the following month. Please note that the information published on our site should not be construed as personal advice and does not consider your personal needs and circumstances. While our site will provide you with factual information and general advice to help you make better decisions, it isn't a substitute for professional advice.

The above table summarizes the average rates offered by lenders across the country. While lower monthly mortgage payments sound enticing, refinancing isn't always a smart financial move. With the lowering of the repo rate, you’re in a favourable position as a property investor in that you’re more likely to qualify for a home loan at a better repayment rate.

You’ll be expected to provide recent pay stubs, often the last two pay periods, that indicate how much you make and prove employment. This can be a good option if you feel ARM rates are likely to stay lower than fixed rates in the future. For example, the 30-year fixed rate has dramatically increased since the start of 2022, which has made the ARM rate a lower, more attractive option right now. Another important consideration in this market is determining how long you plan to stay in the home. People who are buying their “forever home” have less to fear if the market reverses as they can ride the wave of ups and downs. But buyers who plan on moving in a few years are in a riskier position if the market plummets.

No comments:

Post a Comment